Key Takeaways

- Bad credit isn’t the end of your business journey—it’s just a different starting point.

- Microloans, grants, crowdfunding, and revenue-based financing are strong options when banks say no.

- Build business credit alongside your personal recovery to open future funding doors.

- Be cautious of scams and high-interest loans—protect your business’s future.

- Resourcefulness and relationships often matter more than your credit score.

Starting or growing a business can be tough. Add bad credit to the mix, and it might feel downright impossible. But here’s the good news: you can still fund your business—even if your credit score isn’t perfect. In fact, many entrepreneurs have walked this same path and emerged stronger, savvier, and more resilient.

In this guide, we’ll explore real-world funding options, debunk common myths, and give you actionable strategies to keep your business dreams alive—even when traditional banks slam the door.

Table of Contents

Why Credit Scores Matter (But Aren’t Everything)

Credit scores influence the financial world, no doubt. Traditional banks use them to decide if you’re a “safe bet.” A score below 630 is typically considered “bad” by most lenders, and anything under 600—say a 580 credit score—can put up serious roadblocks.

Even if you’ve been a loyal customer with hundreds of thousands in deposits, a big bank may still reject your loan application due to two critical factors:

- Credit underwriting is rule-based: Most big banks use automated systems that still flag a 580 score as too risky, regardless of deposit history.

- Federal regulations: Banks must follow lending standards, and approving a large unsecured loan to someone with poor credit—even if they’re a depositor—can trigger scrutiny or require exception handling.

rigid underwriting rules or federal lending guidelines. At that level, your application might not even make it past automated filters.

But here’s the truth: your credit score isn’t your full story.

Many alternative and online lenders, as well as community banks, are increasingly willing to look beyond your credit score to get a more complete picture of your business’s health and viability. However, “business potential” in this context usually means proven performance, not just projections or estimates written into your business plan. In other words, these lenders typically want to see that your business already exists and has some traction.

They’ll evaluate:

- Your business’s cash flow

- Sales and revenue history

- Collateral or assets

- Your industry

- The strength of your business plan (as supporting evidence, not the foundation)

So while a 580 credit score might stop you at a traditional bank, you could still access capital if your business is up and running, generating revenue, and showing signs of stability or growth.

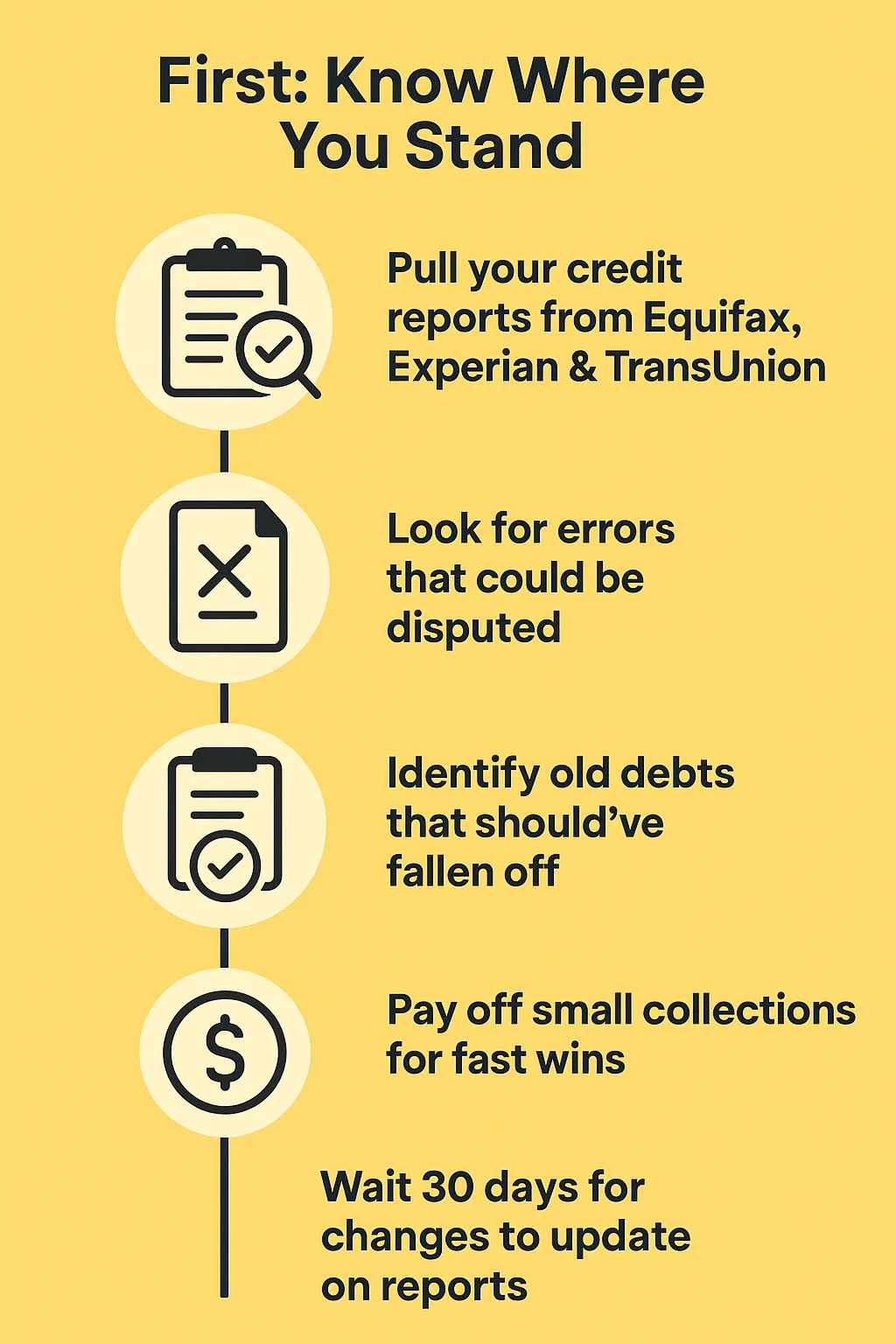

First: Know Where You Stand

Before anything else, pull your credit reports—yes, plural—from all three major credit bureaus: Equifax, Experian, and TransUnion. You’re entitled to a free report from each bureau annually through AnnualCreditReport.com, and it’s a crucial first step.

Carefully review each report and look for:

- Errors that could be disputed (e.g., accounts marked late that were paid on time)

- Old debts that should’ve fallen off (most negative items drop off after 7 years)

- Opportunities for fast wins, such as paying off small collections or reducing credit card balances

Disputing errors or settling small past-due accounts can give your credit score a meaningful bump, but not instantly. Most changes take time to reflect across all three credit reports. Even after you’ve taken action, it can take 30 days or more for your updated credit activity to be processed by creditors and reported to the bureaus. In some cases, you may have to follow up with both the lender and the bureau to ensure corrections were made.

This lag can be frustrating, especially if you’re eager to apply for funding, but it’s important to wait for your credit file to catch up before submitting applications. Otherwise, lenders may still see outdated and inaccurate information.

So be proactive, be patient, and remember: even small credit clean-up efforts can open new doors, but only once they’re fully reflected in your reports.

10 Ways to Fund Your Business With Bad Credit

If you’re trying to fund a business with bad credit, and you don’t have hundreds of thousands in the bank to offer up as collateral—or if your business is still just an idea on paper—then traditional financing routes may feel completely out of reach.

The reality is, many lenders want to see either personal financial strength (like assets or savings) or existing business performance (like revenue and cash flow) before they’ll consider you. But what if you have neither?

Don’t worry—there are still options.

Below are 10 real-world funding strategies that can help you get the capital you need to start or grow, even if your credit score is low and your business is brand new. These options are more flexible, more creative, and often more accessible than a conventional bank loan.

1. Microloans

Microloans are small-dollar loans—usually under $50,000—designed to help early-stage or underserved entrepreneurs access capital when traditional financing isn’t available. These loans are typically provided by nonprofit lenders or Community Development Financial Institutions (CDFIs), which are mission-driven organizations dedicated to promoting economic inclusion and community impact. That means they’re often more flexible with credit requirements, especially for borrowers with low income or bad credit.

When Microloans Are Ideal:

- You’re just starting out and don’t have a long business history or strong revenue yet

- You can’t qualify for a traditional bank loan due to poor credit

- You need a relatively small amount of funding to launch, grow, or stabilize your business

- Your business will provide some social or community benefit, or serve an underserved population

- You have a clear plan and can explain how the money will be used effectively (startup costs, equipment, marketing, etc.)

How Hard Is It to Get a Microloan?

It’s not a walk in the park—but it’s far more accessible than a bank loan if your credit is damaged.

While credit scores are still reviewed, lenders are more concerned with your character, business idea, and motivation. Some microloan providers may consider credit scores as low as 575 or even below, especially if the rest of your application is strong. Many will speak with you directly, help you refine your business plan, and provide coaching or technical assistance along the way.

But make no mistake: it’s still a formal application process. Expect to provide:

- A basic business plan

- Recent bank statements

- Proof of residency or legal status

- A personal guarantee

- Sometimes collateral (though not always)

How Tough Are the Requirements?

Compared to big banks, the bar is lower—but it’s not zero. You’ll need to demonstrate that you’re serious, committed, and have a solid plan for repaying the loan.

Some programs, like Kiva, offer 0% interest loans with no credit check, but require that you bring in a certain number of lenders from your personal network before you go live on their platform.

Other lenders, like the Accion Opportunity Fund, may check credit but weigh your overall profile much more heavily. They often work with people who’ve been turned down elsewhere.

Top Microloan Sources:

- Kiva – Offers 0% interest, no-fee loans up to $15,000 via crowdfunding. No credit check, but requires a social underwriting process.

- Accion Opportunity Fund – Offers personalized support and microloans, even for those with subprime credit.

- Grameen America – Supports low-income women entrepreneurs with no-credit or bad-credit histories.

- Local CDFIs – These are often the best-kept secret in your community. Check your Small Business Development Center (SBDC) or local SCORE chapter for connections.

If you’re willing to put in the effort to build a relationship, prepare your documents, and clearly explain your business vision, microloans can be a powerful stepping stone, not just for funding but for mentorship and long-term support.

2. Business Grants

Business grants are essentially “free money” awarded to businesses that meet specific eligibility criteria. They don’t have to be repaid, which makes them one of the most attractive funding options, especially for entrepreneurs with bad credit.

When Business Grants Are Ideal:

- You’re part of a historically underserved group (e.g., women, minorities, veterans)

- Your business serves a public or community-focused mission

- You’re launching an innovative idea, product, or service

- You can devote time and energy to completing applications

How Hard Is It to Get a Grant?

Grants are very competitive, and most come with detailed application requirements and strict deadlines. You’ll often need to submit a well-structured business plan, financial projections, and sometimes even a pitch deck or community impact statement.

You may apply for many grants before winning one, and the process can feel like a part-time job. But the upside—non-repayable funding—is well worth the effort.

How Hard Is It to Get a Grant?

Grants are very competitive, and most come with detailed application requirements and strict deadlines. You’ll often need to submit a well-structured business plan, financial projections, and sometimes even a pitch deck or community impact statement.

You may apply for many grants before winning one, and the process can feel like a part-time job. But the upside—non-repayable funding—is well worth the effort.

How Tough Are the Requirements?

Requirements vary widely depending on the grantor. Some private or corporate grants may be relatively simple to apply for, while federal or state-level grants often require:

- Business registration and EIN

- Proof of eligibility (demographics, location, purpose)

- A track record of community involvement or innovation

- A strong, mission-aligned business plan

Top Grant Sources:

- Local government or economic development grants

- Federal programs like SBIR/STTR (for tech innovation)

- Private grant competitions from companies like FedEx or Visa

- Minority-, women-, or veteran-focused grants

- Grants.gov – Central portal for federal grant opportunities

- Hello Alice – Offers grant contests and funding for underserved founders

- IFundWomen – Grants and crowdfunding support for female entrepreneurs

Grants take time to apply for and often require a polished business plan, but they’re a lifeline for entrepreneurs with bad credit.

3. Revenue-Based Financing

Revenue-based financing (RBF) provides capital in exchange for a percentage of your future business revenue. Also known as royalty financing or merchant cash advances, it’s not based on your credit score, but on how much money your business brings in. It’s not based on your credit, but on your sales history.

When RBF Is Ideal:

- You have consistent monthly revenue (usually $10k or more)

- You want funding quickly without giving up ownership

- You prefer repayment tied to performance rather than fixed amounts

How Hard Is It to Get?

If your revenue is strong and steady, it’s relatively easy. Approval usually depends on the last 3–6 months of bank statements or POS data. No credit check or minimal credit consideration is involved.

How Tough Are the Requirements?

To qualify, lenders usually require:

- At least 6–12 months in business

- Consistent cash flow

- Proof of sales from invoices, card readers, or bank accounts

While you don’t need perfect credit, you’ll be expected to demonstrate a clear pattern of earnings and ability to absorb daily or weekly repayments.

Be cautious of high fees and repayment terms that may strain cash flow.

Top RBF Providers:

- PayPal Working Capital

- Shopify Capital

- Lighter Capital

- Fundbox

4. Crowdfunding

Crowdfunding lets you raise money from individuals, usually via an online platform, in exchange for rewards, early access, or simply support. It’s a powerful option when your story is compelling and your community is engaged.

Two types:

- Reward-based: You give perks (like early access or products)

- Donation-based: People give to support your cause

When Crowdfunding Is Ideal:

- You have a product, cause, or mission that people can get behind

- Your business is in a creative, social, or consumer-focused industry

- You’re willing to promote your campaign online

How Hard Is It to Get?

It’s not about qualifying—it’s about campaign success. You don’t apply; you create a compelling campaign and try to attract backers. Success depends heavily on your network and marketing efforts.

How Tough Are the Requirements?

Each platform has its own rules. Generally, you’ll need:

- A short video and description of your product/mission

- A strategy for promotion (email list, social media)

- Clear perks or rewards for backers (for reward-based platforms)

No credit check is required—your passion and outreach matter more.

Popular Crowdfunding Platforms:

- Kickstarter – For creative projects and new products

- Indiegogo – Flexible and fixed-funding options

- GoFundMe – Donation-based support, ideal for community businesses

- Fundable – Equity or reward-based crowdfunding for startups

Tips:

- Use a compelling story or video

- Share your mission authentically

- Promote heavily on social media

Credit doesn’t matter here—your story does.

5. Friends and Family

A classic but effective option: ask those closest to you. Borrowing from friends and family can be a straightforward way to raise capital without worrying about your credit score or formal underwriting.

Be transparent about how the money will be used, and consider formalizing the agreement. Use a promissory note or a simple loan agreement. Treat this as seriously as a bank loan to preserve relationships and show professionalism.

When It’s Ideal:

- You have a close network that believes in your idea

- You want flexible repayment terms

- You prefer to keep ownership within your circle

How Hard Is It to Get?

It depends entirely on your relationships. Some friends or relatives may offer funds out of goodwill or belief in you. Others may need reassurance, a clear plan, or even a written agreement.

How Tough Are the Requirements?

It’s up to you and your lender. But it’s strongly advised to:

- Be transparent about how much you need and how you’ll repay it

- Put everything in writing (loan agreement, repayment schedule)

- Avoid mixing personal and business funds without clear records

Pro Tip:

Use platforms like LoanBack or ZimpleMoney to formalize peer-to-peer lending and avoid misunderstandings.

6. Business Credit Cards for Bad Credit

These cards are designed for entrepreneurs with poor or no credit history. They usually come in the form of secured credit cards, where you place a refundable deposit that becomes your credit limit.

Use the card:

- For small, regular purchases

- Pay off your balance in full every month

- Build business credit over time

Eventually, this can help you qualify for higher-limit unsecured cards or credit lines.

When This Is Ideal:

- You need to build or rebuild your credit

- You want to separate personal and business expenses

- You’re starting small and don’t need a large credit line

How Hard Is It to Get?

Secured cards are relatively easy to get approved for, even with a score below 580. Unsecured cards with low credit requirements are harder but still available.

How Tough Are the Requirements?

To qualify, you’ll usually need:

- A refundable security deposit ($200–$2,000+)

- A legal business entity and EIN (for business cards)

- Some basic documentation (business address, bank account)

Notable Options:

- Capital One Spark Classic (for fair credit)

- Discover It Secured (personal but useful for early-stage startups)

- OpenSky Secured Visa (no credit check)

- Brex (for startups with strong cash flow but no personal guarantee)

7. Personal Loans from Online Lenders

Even if banks say no, online lenders like Upstart or LendingClub may approve you for a personal loan, especially if you have stable income or a co-signer.

When This Is Ideal:

- You have a regular paycheck or side income

- Your business is pre-revenue and needs launch capital

- You need a quick approval process

When This Is Ideal:

- You have a regular paycheck or side income

- Your business is pre-revenue and needs launch capital

- You need a quick approval process

How Hard Is It to Get?

If your credit is in the mid-500s to low 600s, some platforms will still consider you. Factors such as income, employment, and education can help offset a poor credit history.

How Tough Are the Requirements?

Each lender is different, but generally you’ll need:

- Proof of income (W-2s, pay stubs, or tax returns)

- A credit score of 580 or higher

- A U.S. bank account and ID

Loan amounts range from $1,000 to $40,000, and APRs can be high, so compare offers carefully. While not ideal for large capital needs, a $5,000–$20,000 loan can give you enough to start lean.

Trusted Lenders:

- Upstart – AI-based lending considers education and job history

- LendingClub – Peer-to-peer lending with soft credit check

- Avant – Specializes in loans for lower credit scores

- SoFi – Better for higher credit scores but offers good terms

8. Equipment Financing

Need gear, machines, or vehicles? Equipment financing uses the item itself as collateral, making credit less critical. This type of financing lets you buy or lease business equipment, using the equipment itself as collateral, reducing the lender’s risk.

Lenders care more about:

- The resale value of the equipment

- Your ability to repay over time

Even if you have bad credit, if the equipment is critical to business operations, many lenders will still consider your application.

When This Is Ideal:

- You need to purchase essential equipment (e.g., trucks, computers, ovens)

- You have a bad credit score but can offer a down payment

- Your business relies heavily on physical tools or machinery

When This Is Ideal:

- You need to purchase essential equipment (e.g., trucks, computers, ovens)

- You have a bad credit score but can offer a down payment

- Your business relies heavily on physical tools or machinery

How Hard Is It to Get?

Easier than traditional loans, because the equipment secures the deal. Lenders are primarily concerned with the value of the equipment and your ability to make payments.

How Tough Are the Requirements?

Expect to provide:

- A vendor quote or invoice for the equipment

- Basic business and financial information

- Sometimes, a personal guarantee or a small down payment

Even with a credit score in the 500s, you may be approved.

Equipment Lenders to Explore:

- Crest Capital

- National Funding

- Taycor Financial

- Balboa Capital

9. Invoice Factoring

Invoice factoring turns your unpaid invoices into cash by selling them to a factoring company, which advances you 70–90% of the invoice value upfront. If your business invoices clients and waits 30–90 days to get paid, you can “sell” your invoices to a factoring company for immediate cash.

You’ll typically receive:

- 70–90% upfront

- The rest (minus fees) when the invoice is paid

Since the factoring company collects from your clients, your credit isn’t a big factor.

When This Is Ideal:

- You run a B2B business with net-30 or net-60 payment terms

- You need to bridge cash flow gaps while waiting for customers to pay

- Your clients are reputable and reliable

How Hard Is It to Get?

It’s easier than a loan. Since the factoring company collects from your clients, your credit isn’t the main concern—they care more about your clients’ creditworthiness.

How Tough Are the Requirements?

To qualify, you typically need:

- A few active invoices totaling at least a few thousand dollars

- Business and client verification

- Transparent invoicing practices

Factoring can be fast (sometimes same-day funding), but fees vary.

Factoring Providers:

- BlueVine

- altLINE

- FundThrough

- TCI Business Capital

10. Partner with Someone Who Has Good Credit

This is more about relationships than lenders: partnering with someone who has better credit or assets can help your business get off the ground. If you have a trusted partner, spouse, or co-founder with stronger credit, they could:

- Co-sign a loan

- Apply for funding on behalf of the business

- Use their creditworthiness to get better rates

This is a big ask, so build trust and ensure clear expectations are set in writing.

When This Is Ideal:

- You have a trusted co-founder or spouse with good credit

- You’re open to sharing ownership or responsibility

- You need someone to co-sign or personally apply for loans or cards

How Hard Is It to Get?

It’s not about approval; it’s about finding the right person and building trust. If they’re willing to lend their name or credit, it can drastically increase your options.

How Tough Are the Requirements?

It depends on the arrangement. You may need to:

- Draft a formal agreement outlining roles and responsibilities

- Legally form a partnership or corporation

- Clarify who’s liable for what

Done right, this can lead to faster access to capital and stronger financial backing.

Tip:

Only enter financial partnerships with people who share your values and business vision. Trust is more important than credit in this case.

Building Business Credit (While You Fund)

Funding with bad credit is just the start. Your long-term goal should be building strong business credit, which is separate from your personal score.

Steps to take:

- Register your business with Dun & Bradstreet

- Get a D-U-N-S Number

- Open a business bank account

- Use vendors that report to business credit bureaus

- Pay on time—always

Strong business credit means more funding options later and better rates.

What to Avoid When You Have Bad Credit

Loan Scams

Beware of “guaranteed approval” pitches or lenders asking for upfront fees. If it sounds too good to be true, it usually is.

High-Interest Predatory Loans

Some lenders target people with bad credit by charging triple-digit APRs. These loans may seem like a lifeline but often trap entrepreneurs in debt cycles.

Always:

- Read the fine print

- Ask about APR, fees, and repayment schedule

- Compare at least 2–3 lenders before committing

Payday Loans

While tempting in a financial crunch, payday loans are one of the riskiest options for funding your business. These short-term loans come with astronomical interest rates and must be repaid quickly, usually within two weeks. If you miss a payment, fees and rollovers can spiral into unmanageable debt. Payday lenders often do not report to credit bureaus, so using them won’t even help build your credit. If you’re serious about growing a business, skip the payday trap and look for more sustainable funding options.

Real Talk: Success Stories Exist

Many successful founders—like Daymond John (FUBU) or Barbara Corcoran (The Corcoran Group)—started with bad credit or no financial backing. What got them through?

- Resourcefulness

- Creativity

- Relationship-building

- Smart money moves

You don’t need perfect credit to be a great entrepreneur. You need persistence and a willingness to explore all your options.

FAQs

Can I get an SBA loan with bad credit?

It’s possible—but challenging. Most SBA loans require a credit score of 650 or higher. However, some community lenders or microlenders offering SBA Microloans are more lenient with credit requirements. If you can demonstrate strong business potential, cash flow, or collateral, you may still qualify. Consider pairing your application with a co-signer or exploring SBA-affiliated nonprofit partners that are more flexible. Ultimately, while an SBA loan may not be your first option with poor credit, it can be worth revisiting once you’ve rebuilt your score or business profile.

How do I improve my chances of getting a loan with bad credit?

Start by applying for loans designed for low-credit borrowers, such as microloans or revenue-based financing. Strengthen your application by showing solid business income, providing a detailed plan, and offering collateral. You can also consider adding a co-signer with better credit. Clean up your credit report by disputing errors, paying off small debts, and avoiding new hard inquiries. If possible, build a positive track record with a secured business credit card. These steps won’t guarantee approval, but they significantly increase your odds of securing funding.

Is it better to wait until my credit improves before starting my business?

Not necessarily. If you have a solid business idea, a supportive network, and non-traditional funding options, you may be able to start lean and build as you go. Many entrepreneurs use bootstrapping, crowdfunding, or friends-and-family funding to launch—even before their credit rebounds. However, if your business model requires large capital investment and lenders are your only hope, it may be wise to spend 3–6 months improving your credit before applying. It comes down to your specific financial situation and risk tolerance.

What’s the difference between personal and business credit?

Personal credit is tied to your Social Security number and reflects how you manage personal debt (like credit cards and loans). Business credit, on the other hand, is linked to your Employer Identification Number (EIN) and tracks how your business pays suppliers, creditors, and lenders. Building business credit can help you separate finances, qualify for better financing terms, and reduce risk to your personal assets. Even with bad personal credit, strong business credit can eventually open new doors.